Tax is not a technical revenue collection activity of the modern state. Tax is the most naked political tool that shows who the state favors, which classes it protects and which groups it makes pay the price. Therefore, taxation is not a matter of fiscal technique, but of the constitution, regime and class politics. The issue that needs to be discussed in Turkey today is not whether taxes are “high” or “low”; it is who they are imposed on, at what cost and with what political logic.

Tax is not a technical revenue collection activity of the modern state. Tax is the most naked political tool that shows who the state favors, which classes it protects and which groups it makes pay the price. Therefore, taxation is not a matter of fiscal technique, but of the constitution, regime and class politics. The issue that needs to be discussed in Turkey today is not whether taxes are “high” or “low”; it is who they are imposed on, at what cost and with what political logic.

The taxation system in Turkey is formally based on Article 73 of the 1982 Constitution. This article stipulates that taxation shall be imposed for the purpose of meeting public expenditures within the framework of the principles of legality, fiscal power, generality, equality and fair and balanced distribution of the tax burden. This provision must be read in conjunction with the principles of the rule of law, social state and legal security, which are derived from the constitution as a whole. However, the problem in Turkey is not the lack of constitutional principles. The problem is that these principles have been politically suspended. The tax regime is not the result of the social state of law model envisioned by the constitution; it is the product of another economic and political mind positioned against it.

At this point, the main issue to be underlined is the following: The tax regime in Turkey is the product of a political choice, not a constitutional imperative. While the Constitution mandates taxation according to financial power, the practice targets citizens with indirect and regressive taxes on consumption. Rather than a constitutional violation, this situation amounts to a dysfunctionalization of the constitution. The legal text remains in place, but the political power neutralizes it through fiscal policy. Thus, the constitution ceases to be a normative framework and is reduced to a symbolic document.

Liquidation of the Social State Principle through Taxation

A social state is not just a state that distributes aid. A social state is a state that balances inequalities created by the market through taxation. Tax is the main instrument of this balance. If a tax system does not correct the distribution of income and wealth, but rather distorts it, the principle of the social state has effectively disappeared.

This is exactly what tax policy in Turkey does. The tax burden is systematically shifted to the consumption of citizens through indirect taxes. This is not a mistake. It is a conscious choice. Because indirect taxes are politically comfortable. They spread to a broad base, individualize the reaction, and do not disturb capital. And society pays the price.

The expression “liquidation of the welfare state” is not figurative here. When the tax system eliminates the redistributive function of the social state, the state is reduced to a mere revenue-collecting apparatus. Taxes are used not for financing public services, but for the management of budget deficits and the sustainability of the economic order established in favor of capital. In this case, tax becomes the instrument not of the social contract between citizens and the state, but of the hierarchical relationship between power and society.

Evisceration of the Principle of Equality in Taxation

Article 10 of the Constitution enjoins equality before the law, and Article 73 requires that taxes be levied according to financial ability. Equality in taxation does not mean taxing everyone at the same rate. Equality in taxation means taxing everyone according to their ability to pay. The realization of this principle is the responsibility of the legislative body.

In Turkey, however, the legislature does not use this power to ensure tax justice, but in line with political and class priorities. With exemptions, exceptions, incentives, amnesties and temporary reductions, the tax system has ceased to be a mechanism that ensures equality.

This structure shows that tax privilege, not tax equality, has been institutionalized. Instead of strengthening the principle of equal citizenship, the tax system deepens the distinction between capital and citizens. While the principle of equality continues to exist in texts, in practice it has been replaced by selective protectionism.

The Truth in Numbers

Approximately 65-70 percent of total tax revenues consist of indirect taxes. Value Added Tax and Special Consumption Tax together account for about half of total tax revenues. In contrast, the share of corporate tax is only 10-12 percent. A significant portion of income tax is not based on declaration but on deductions from wage earners at source.

This table shows that the tax burden is not on capital, but on the daily lives of citizens.

However, it is insufficient to read this table only as a numerical imbalance. These figures clearly reveal the class character of taxation. Indirect taxes create a disproportionate burden on low-income groups as they are levied on everyone at the same rate regardless of income level. This makes the tax system regressive and distorts income distribution.

Where Does Tax Start? In Citizen's Life

In Turkey, taxation starts in life, not in profit. Citizens are taxed with withholding tax before they earn their income. As soon as they spend their earnings, they are taxed a second and third time. Therefore, the tax burden does not appear on company balance sheets, but in the kitchen, on the invoice, on the debt.

Tax is not an abstract financial burden for citizens; it is a constant companion of everyday life. The state reaches directly into the citizen's pocket when the electricity switch is pressed, the stove is turned on in the kitchen, the phone is touched, the car is driven. For capital, on the other hand, tax is an item that can often be deferred, reduced or eliminated altogether through accounting techniques.

The Concrete Anatomy of the Tax Burden: Money Flowing from the Citizen's Pocket to the State

Citizen Buying a Car

Tax-free vehicle price is 500.000 TL. *

SCT 80 percent: 400,000 TL.

VAT 20 percent on the amount including SCT: 180,000 TL.

Total tax is 580.000 TL.

The sale price is 1.080.000 TL.

The citizen pays more taxes to the state than the car.

Citizen Receiving a Phone Call

Tax-free price is 30.000 TL. *

SCT 50 percent: 15,000 TL.

VAT: 9.000 TL.

Other shares are approximately 1,000 TL.

The total tax is approximately 25,000 TL.

You pay as much tax as the phone itself.

Citizen Buying a House

The new house price is 2.000.000 TL. *

VAT 10 percent: 200,000 TL.

Title deed fee 4 percent: 80,000 TL.

Other fees are approximately 10.000 TL.

The total initial tax burden is approximately TL 290,000.

Property tax, environmental cleaning tax and VAT on invoices follow.

Electricity, Water, Natural Gas

Taxes and funds on electricity are 18-20 percent.

VAT on natural gas is 20 percent.

The total load on the water is about 20 percent.

Citizens pay taxes because they live.

Fuel

Approximately 40-45 percent of the pump price of fuel is composed of indirect taxes such as SCT and VAT.

(FIGURES ARE GIVEN AS AN EXAMPLE)

What does the Company Pay?

On paper, corporate tax is 25 percent.

With exemptions, incentives, amnesties and restructuring, the effective rate falls below 10 percent.

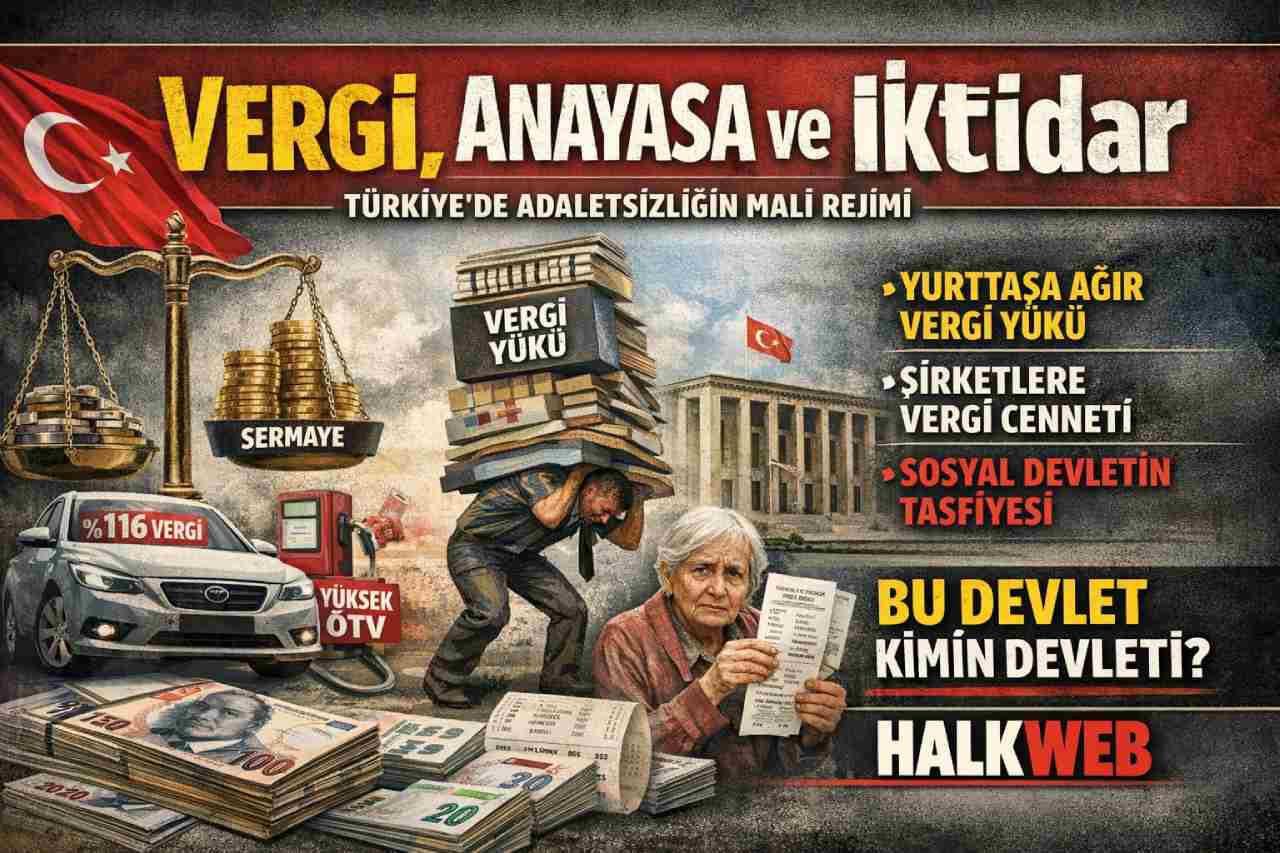

While the citizen pays 116 percent tax on a car, the company pays 10 percent on profits.

This comparison is the most naked indicator of tax injustice. The tax levied on the citizen's consumption is absolute and inevitable. Corporate profits, on the other hand, are negotiable, deferrable and often protected by politicized mechanisms.

The Conscious Break with the OECD and the Neoliberal Regime

In OECD countries, the share of indirect taxes is 30-35 percent on average. Corporate and wealth taxes are the backbone of the system. In Turkey, this structure is reversed. This is not backwardness; it is a conscious regime choice. Neoliberalism does not shrink the state; it changes who the state protects. In Turkey, the state has withdrawn from capital and settled in the lives of citizens.

This preference stems not from an economic necessity but from a political orientation. The tax regime is designed as a tool that accelerates capital accumulation and disciplines labor and consumption. Therefore, the tax system in Turkey is not an economic technique but a mechanism of class domination.

Tax Amnesty, Electoral Economy and the Collapse of Legal Security

Tax amnesties have ceased to be an exception and have become a routine tool of the electoral economy. This situation destroys tax morality, erodes legal security and penalizes taxpayers. Tax ceases to be a public responsibility and turns into a deferrable debt.

Tax amnesty destroys predictability, one of the most fundamental principles of the rule of law. The state itself declares that the rules are temporary. This destroys not only the fiscal system but also the sense of social justice.

Informal Economy: Chronology of Conscious Tolerance in Turkey

In Turkey, the informal economy is not a temporary aberration, but an ongoing practice of governance. With the January 24 decisions, controls were loosened, informal employment was tolerated, and amnesties were normalized. Borrowing was preferred in the 1990s, the incentive regime was expanded in the 2000s, and restructuring became permanent after 2010. The informal economy is not a failure, but a managed choice.

Solution: Political Rupture, Not Reform

This system cannot be fixed by technical adjustments. A social state cannot be established without shifting the tax burden to corporations, big capital and wealth.

Corporate income tax should be made the main carrier of the budget.

Exemptions and exemptions should be eliminated.

Wealth and large property taxes should be imposed.

Rent sectors should be taxed extraordinarily.

Profit leakage by multinational companies must be prevented.

VAT and excise duties on water, food, energy and communications should be abolished.

These are not technical proposals; they are political choices. Without the realization of these preferences, there can be no talk of tax justice, social state and equal citizenship.

Conclusion

- The tax regime is not a fiscal issue, but a government choice.

- The problem in Turkey is not wrong rates, but conscious injustice. Tax is levied on life, not profit.

- Capital is protected and citizens are disciplined. While the constitution mandates a social state, fiscal policy de facto dismantles it.

Equal citizenship is in the texts but not in the budget. Indirect taxes perpetuate poverty and produce politelessness. - Tax amnesties corrupt the law, incentives corrupt justice and informality corrupts the state. This picture is not a malfunction, it is a functioning regime.

- The tax system is not broken; it has been correctly chosen to work against whom. There is no social state without tax justice.

- There can be no democracy without a welfare state. The question is not technical. The question is political: Whose state will this state be?